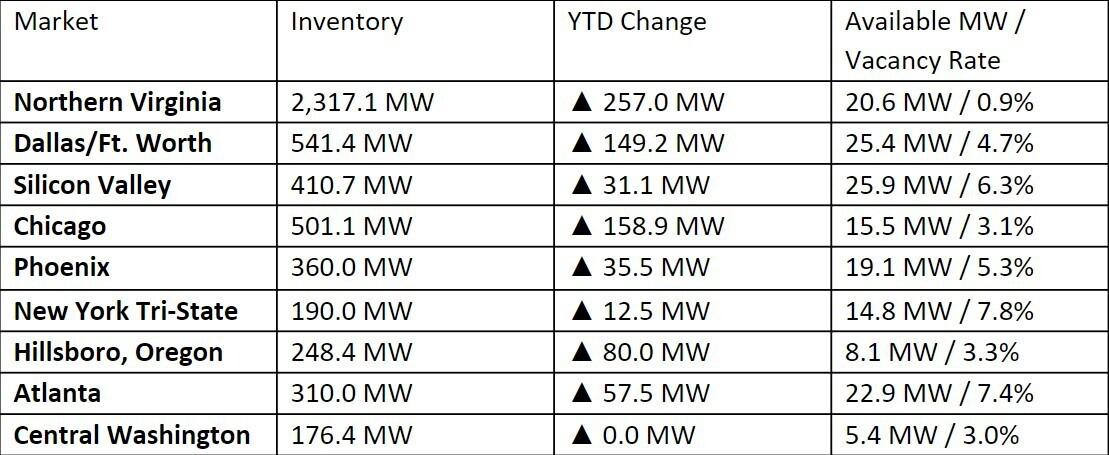

Inventory in America’s Top 10 Data Center Markets (Q3 2023)

In the table above, provided by CBRE, we see that available inventory of data center space and power in major markets is at a historic low. Even as providers continue to add capacity (YTD Change), they face ongoing shortages of available power and extremely low vacancy rates in their facilities.

To cite just one example, America’s largest data center market – Northern Virginia – has an inventory of 2,317.1 megawatts (MWs). In 2023, this regional market added 257 MWs of new capacity. But as of Q3 2023, the entire market only had 20.6 MWs of available power, and a vacancy rate of less than 1%.

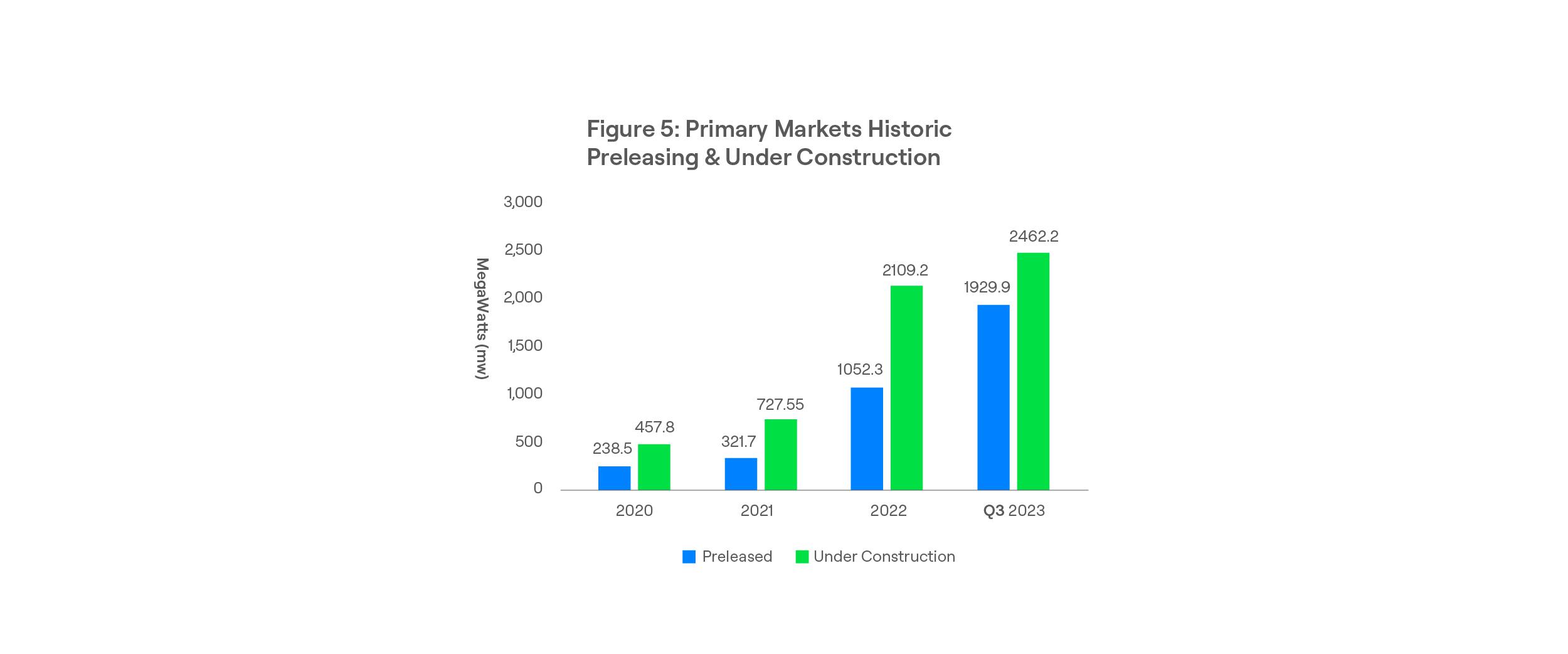

This is why pre-leasing has become essential. Many companies are now reserving space and power in data centers that haven’t even been built yet.

Welcome to the AI Boom

There’s little mystery as to one of the primary factors driving this trend and creating this unprecedented demand: the emergence of a rapidly building Artificial Intelligence market.

AI is not considered “just another new technology.” It’s being called a “game changer.” Some high-tech industry experts are predicting that AI may be even bigger in the 2020s than the Internet was in the 1990s. Sundar Pichai, the CEO of Alphabet, has gone so far as to claim that it’s “more profound than fire, electricity or anything that we have done in the past.”

The rise of AI has been enabled by High-Performance Computing (HPC), and AI workloads require IT deployments with massive amounts of compute capacity. But these deployments can’t exist in a vacuum– they must live somewhere on our planet, in data centers.

As hyperscalers and IT enterprises invest vast amounts of money and resources in AI, they are actively seeking data centers to support their HPC deployments. But many of those facilities don’t exist yet, except in architectural plans. Consequently, companies are reserving future space and power through pre-leasing agreements with data center providers.